The preapproval checklist 2025 is still one of the most important steps before you start touring homes.

If you are touring homes before getting preapproved, stop.

In 2026, sellers still expect proof of qualification before accepting an offer.

While some preapproval checklist 2025 searches may feel outdated, the fundamentals remain critical.

In the Houston buyer’s market 2026, buyers with full documentation move faster and negotiate stronger.

You are going to want this handled before falling in love with a house.

Why the Preapproval Checklist 2025 Still Matters in 2026

Even in a buyer-leaning market:

- Sellers want certainty

- Builders require lender approval

- Appraisals require financial stability

- Closing timelines must be realistic

Market context: https://redefinedhtx.com/blog/houston-buyers-market-2026/

Without full underwriting review, you are guessing.

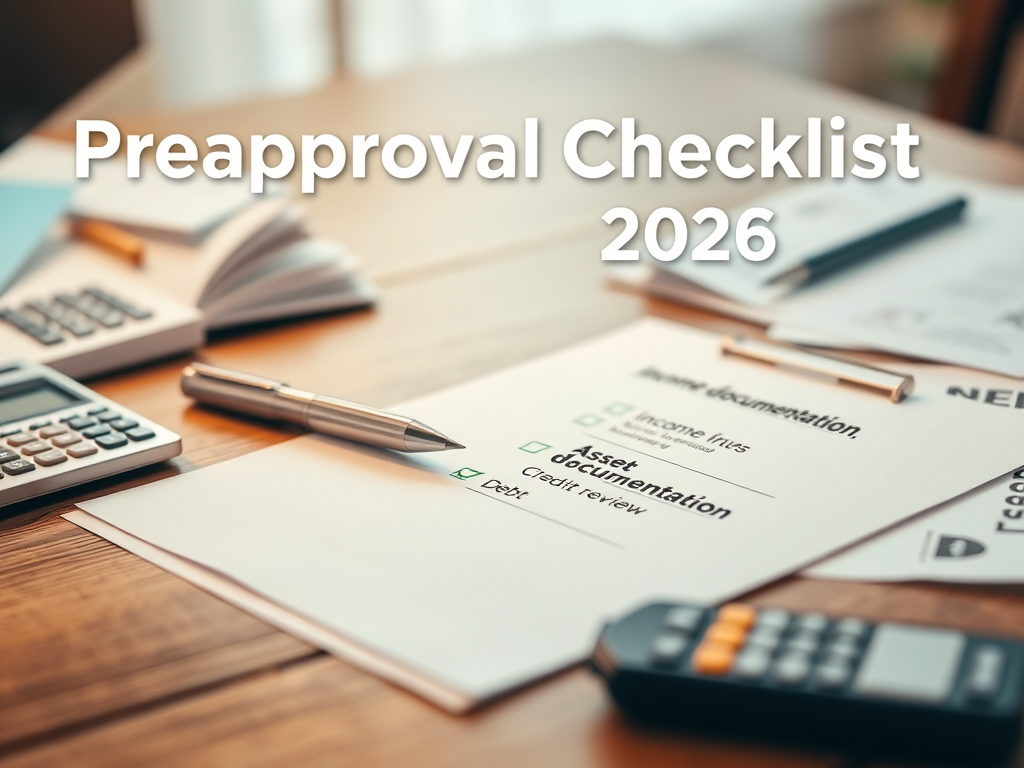

The Updated Preapproval Checklist 2025 Buyers Still Need

Here is what lenders typically require:

Income Documentation

- Two recent pay stubs

- Last two W-2s

- Two years of tax returns if self-employed

Asset Documentation

- Two months of bank statements

- Retirement account statements if using for reserves

- Gift letter documentation if applicable

Credit Review

- Pull of tri-merge credit report

- Explanation letters for recent late payments

- Verification of disputed accounts

Debt Review

- Current monthly obligations

- Student loan balances

- Auto loans and credit cards

Consumer Financial Protection Bureau resource: https://www.consumerfinance.gov

Self-Employed Buyers Need More

If you own a business, expect:

- Two years of full tax returns

- Profit and loss statements

- Business bank statements

- Year-to-date income verification

For income structure insight: https://redefinedhtx.com/blog/home-loans-for-self-employed-in-texas/

Net income, not gross revenue, determines qualification.

Common Mistakes That Derail Approval

Buyers often:

- Open new credit cards mid-process

- Finance furniture before closing

- Change jobs

- Deposit large unexplained cash sums

- Miss payments during underwriting

Once preapproved, financial behavior must remain stable until closing.

What a Complete Preapproval Checklist Includes

Not all preapprovals are equal.

A strong preapproval includes:

- Full credit review

- Verified income documentation

- Verified assets

- Debt-to-income calculation

- Automated underwriting approval

A quick online letter without documentation can collapse during escrow.

How the Preapproval Checklist Affects Negotiation Power

In 2026, sellers are negotiating more.

But they still prefer:

- Fully underwritten buyers

- Clear financing timelines

- Realistic closing dates

Preparation increases leverage.

For first-time buyer strategy: https://redefinedhtx.com/blog/how-to-buy-a-house-in-texas/

Timing Your Preapproval

Preapprovals are typically valid for:

- 60 to 90 days depending on lender

- Credit refresh may be required

- Updated pay stubs often needed

Plan your house search within that window.

At The Musto Group, Jessica Musto and Donato Musto align real estate strategy with financing structure from the beginning.

We evaluate your numbers before showing homes so your search stays realistic and competitive.

If you are still Googling preapproval checklist 2025, it is time to move from research to readiness.

Review your documents.

Confirm your budget.

Lock in your buying range.

Visit our contact page to start your preapproval strategy with our team.

Sources

Consumer Financial Protection Bureau – https://www.consumerfinance.gov

Fannie Mae Selling Guide – https://singlefamily.fanniemae.com

Freddie Mac Loan Guide – https://guide.freddiemac.com

Houston Association of Realtors – https://www.har.com

Proudly Serving: Tomball, The Woodlands, Cypress, Spring, Hockley, Katy, Conroe, Willis, Kingwood, New Caney, Porter, Magnolia, Plantersville, Waller, Rosenberg, Richmond, Houston, & surrounding areas across Harris County, Montgomery County, Fort Bend County, Waller County, San Jacinto County, Liberty County, Grimes County & Walker County.

Leave a Reply